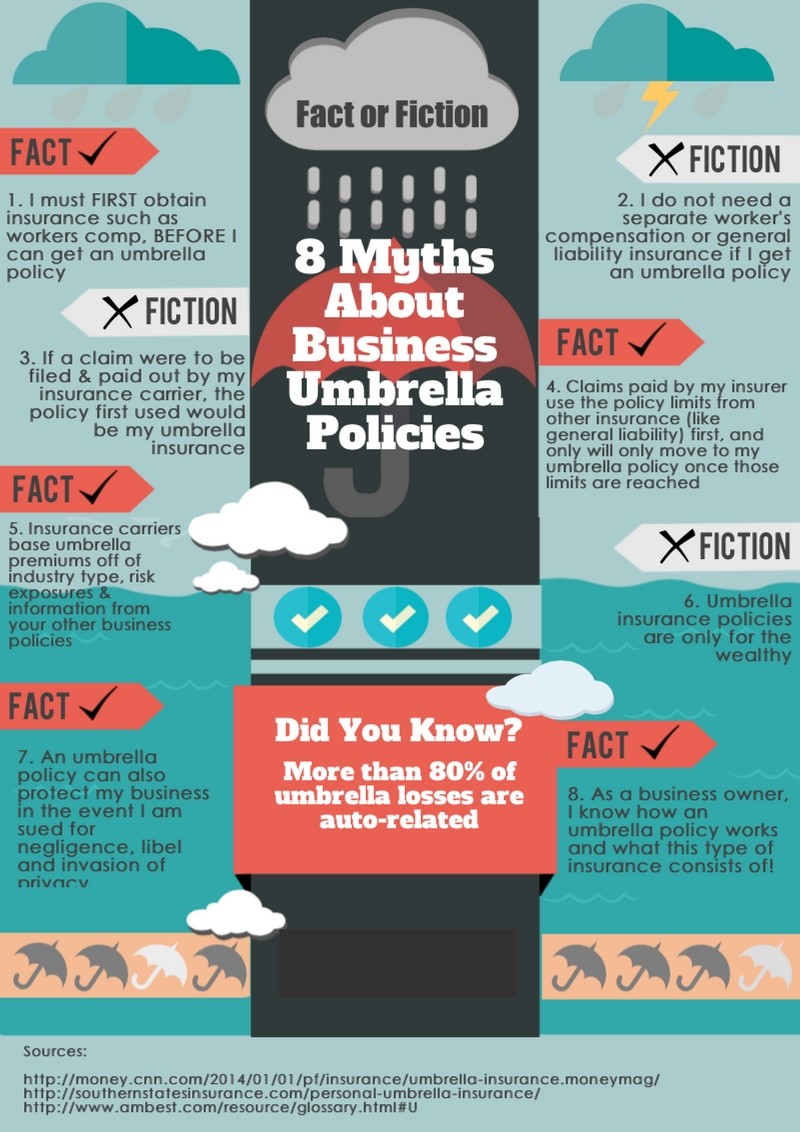

You’re cautious, you’ve made sure to be properly insured. You have talked to your insurance provider and secured all of the protections suggested. Yet, do you feel confident about avoiding financial ruin if you accidentally cause major injuries? Or property damage to others? Your insurance limit may be reached in some cases. If you are sued for the remaining losses, how will you react? That’s where a personal umbrella policy comes in.

An umbrella policy is sometimes referred to as excess liability insurance. Think of it as a fail-safe for your savings and other assets. If you’re sued for damages that exceed the liability limits for your homeowners, car or other coverage, an umbrella policy will pay what you owe. Protecting your savings and assets, it’s a great addition to your current policies. Keep in mind there are underlying limits that are required to be eligible for an umbrella policy. You must have liability coverage for your homeowners least 300K, for auto the minimum is 250K and motorcycle the minimum is 500k.

Who Needs An Umbrella Policy?

Umbrella insurance, although not required it is a valued investment. It’s commonly purchased by individuals who own property, volunteering, have significant savings or other assets, and those who own things that can lead to injury lawsuits like pools, trampolines, and dogs. Those are only a few examples. Anyone can benefit from umbrella insurance.

A lawsuit could clean out your current savings and in common cases, it can claim your earnings in the future. Don’t think because you don’t have the money now, there’s no way to retrieve the losses later. You could be stuck paying off the debt for years.

What An Umbrella Policy Pays For:

-

- Others’ injury treatment and funeral costs.

- Others’ property damage.

- Lawsuits involving slander, libel, defamation of character and other personal attacks.

- Your legal defense costs.

- Injuries or property damage suffered by a tenant if you’re a landlord.

What An Umbrella Policy Doesn’t Pay For:

-

- Your own injuries.

- Damage to your personal belongings.

- Others’ injuries or property damage that your business is liable for.

- Intentional or criminal acts.

- Property damage or injuries you cause while using certain recreational vehicles, such as an all-terrain vehicle or Jet Ski (this can vary by insurer).

Buying Umbrella Insurance

Now that you have a better understanding, let’s get to the easy part. BUYING. It’s best to buy enough coverage to cover your net worth. Include your savings, other assets, and income. Think about including your potential income too if you’re likely to earn significantly more in the near future.

Umbrella policies usually start with $1 million in coverage, even with the minimum protection you still have a decent amount of coverage. When buying ask us about the companies limits to be well informed if you need additional coverage in the future. Most umbrella policies with a $1 million in coverage can range from approximately $150 to $300 a year, according to the Insurance Information Institute. In this litigious society of ours, the extra cost is well worth the peace of mind you get knowing your assets are protected from lawsuits.